Share this Post

I haven’t talked about it much on the blog, but I recently made a career move and jumped ship to a new E&P. If you want the details you can easily look me up on linkedin. Hopefully it turns out to be a good move for my career.

In the meantime, I thought I could talk a bit about what you should do (and what I did) with my investments when I made the change.

First thing I did was contact Vanguard and cash out my 401k and send it over to Tradeking (affiliate link) to be put in my traditional IRA. I think Vanguard is a great company, but moving it to an IRA vastly expands my investment options and lets me pick individual stocks and a more diverse, lower fee set of ETF’s.

If you don’t have a trading account set up. I highly recommend Tradeking. It’s what I personally use for my regular IRA, Roth IRA, and trading account. The interface is smooth and intuitive, customer service has responded to my questions every time, and it’s cheap ($4.95 / trade).

Once that cash hits I’ll start allocating it out to dividend payers, and probably some ETF’s – specifically some international stuff where I’m under allocated.

The new 401k is with Fidelity. I’m sure they’re high quality as well, but I’m used to Vanguard and a little bummed about the change.

First thing was to set my contribution to max out my 401k for the year. There’s 18k in the bank. I won’t give all the details, but there is a pretty solid company match, so I should see satisfying growth in that account. As always I mentally reference my savings hierarchy and fully funding my 401k is at the top of the list.

Next thing to do was evaluate my fund options. So what did I take in to consideration?

Asset Allocation

Most 401k’s will have a mix of stock and bond funds, though it’s usually pretty limited per asset class. I expect you will have a couple of US large cap, mid cap, and small cap. In addition there’s often one or two international funds. Unfortunately, most available funds won’t be the lowest cost and anything but US large domestic, will tend to be expensive.

Fees

Like Buffett told us, fees are the killer of performance and end up mattering more than allocation. That’s why my main focus is on what are the lowest cost options available in Fidelity?

My Strategy

Because I’ve managed to accumulate a decent portfolio outside my current 401k, I don’t really worry about having the most diverse allocation. I choose to focus on what I deem to be a more important factor and work the rest of my portfolio around the limitations of my 401k.

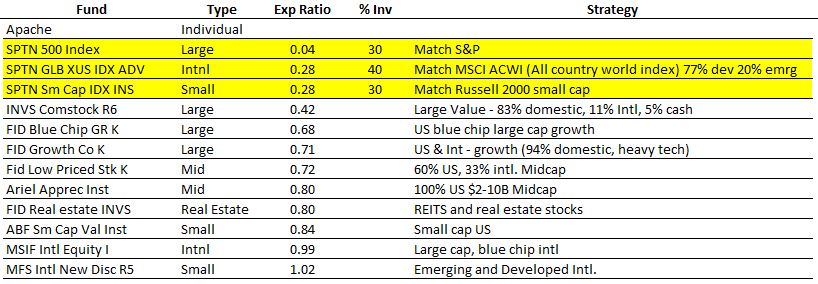

I threw the list into excel with a couple of basic characteristics and sorted by expense ratio. As you can see there is only 1 bare bones fee fund that tracks the S&P. I was really tempted to just put that at 100% and call it done. However there were 2 runner ups that while not .04%, were still quite low cost at 0.28% that provide a decent level of diversification internationally and among small caps. I went ahead split my entire allocation between the three.

Because my company periodically grants stock, I chose not to put any additional funds into company stock in the 401k. I’m already way, way to heavy energy.

The New Job Market

July 28, 2017Munger: The Psychology of Human Misjudgement

June 26, 2017Millennials are Holding Too Much Cash

June 25, 2017Share this Post