Share this Post

I recently rolled my old 401k in to my IRA after making a job change. So I’m flush with cash!

So what to do? The market in the US is way up the past few years so that gives me a bit of pause on where to throw my money. Because it’s in an IRA there are really only a couple of options:

Broad Allocation

- Hold all cash. Wait for a bust.

- Hold portion of cash (20% for example) invest the rest.

- Invest domestically (ETF or stocks)

- Invest foreign developed (ETF or stocks)

- Invest emerging markets (ETF or stocks)

- I’m ignoring bonds. No interest based on current rates.

Asset Choice

- Individual stocks

- ETFs

Timing

- All at once

- Multiple Allocations over time

Why International?

The bulk of my 401k already goes to domestic ETF’s, so I’m using my IRA rollover to get the bulk of my international exposure. I plan to make my purchases in 4 parts. I’m not trying to time the market, just spread my risk of putting all my money to work at the exact wrong moment before a bust. I’ve got calendar reminders every month to revisit and determine if it’s time for a purchase, while having a plan of doing so quarterly.

I’m also looking to substantially raise my international exposure due to the US’s impressive run-up the past few years that has largely not occurred in internationally. Valuations and dividend rates are higher almost across the board outside the US and the strong dollar allows purchases at a discount to historical currency levels.

While I still may choose some individual international stocks, like my personal favorites, Nestle and Diageo or oil exposure in BP and Shell, the bulk of my exposure will be through some broad based ETF’s for simplicity sake.

Research

So how to pick those funds? I dug into some databases provided by ETFDB, took a number of data dumps and did some sorting and filtering by my primary criteria:

- Composition by country

- Fee Level

- Dividend Level

So how did I determine what I wanted? First of all I was looking for hte lowest feels possible.

Once I had that sorted down and I had found the top 10 or so that interested me, I dug in to the details of each fund. The image below is sorted on Expense Ratio.

I didn’t realize how much Vanguard would dominate my options. They’re clearly the leader in all the international categories by expense ratio.

I like VEA a lot, as well as VGK, but they are Europe and Europe Pacific specific. I already complicate my life enough with individual stocks, so all else equal, I’d prefer a single fund for exposure. That leaves VXUS versus VEU. At first glance these 2 funds look identical. The key is understanding the difference in the 2 indexes. Let’s see how they stack up.

Most stats are pretty spot on. Major difference is the number of stocks and the market cap. That’s the key. What about composition of the holdings?

VXUS

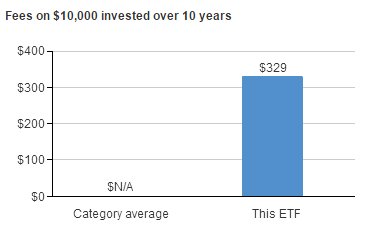

Let’s see a couple more visuals on the fund we decided to go with.

{kind=link}

Taxes

There is one major disadvantage of having the bulk of your financial assets in tax deferred accounts (401k/IRA). International investing penalizes you, if the company in which you are investing doesn’t have tax treaties in the US. You are likely paying taxes on those jurisdictions that you can’t get back.

A prime example is Nestle. I currently only have enough in my IRA to make a substantial purchase as my brokerage dollars are allocated elsewhere. However, I’m a bit loathe to do so, since I’ll be forced to pay taxes on those dividends regardless of their home in my tax free IRA.

If you have the funds, it’s smarter to steer your taxable assets toward those countries, allowing you to take a credit against your own US taxes. However if the bulk of your assets are in you 401k/IRA it still makes sense to get international exposure, even calculating in the tax issue.

If you have both a traditional IRA and a Roth, be sure to use the Traditional as it will reduce your future tax bill, while in the Roth your just permanently out that money.

Conclusion

I’ll be continuing to make substantial international investments through VXUS and select individual stocks. I hope my analysis helps you decide how to evaluate ETF’s and consider some international diversification.

If you have any thoughts on my process, let me know in the comments.

The New Job Market

July 28, 2017Munger: The Psychology of Human Misjudgement

June 26, 2017Millennials are Holding Too Much Cash

June 25, 2017Share this Post